Understanding Credit Cards

A credit card is a multifaceted financial instrument that enables cardholders to borrow funds from banks or financial institutions to pay for purchases, comprising both goods and services. These cards function as a form of short-term borrowing where users are obligated to reimburse the borrowed amount. This repayment often includes interest, contingent upon the terms specified by the issuing entity.

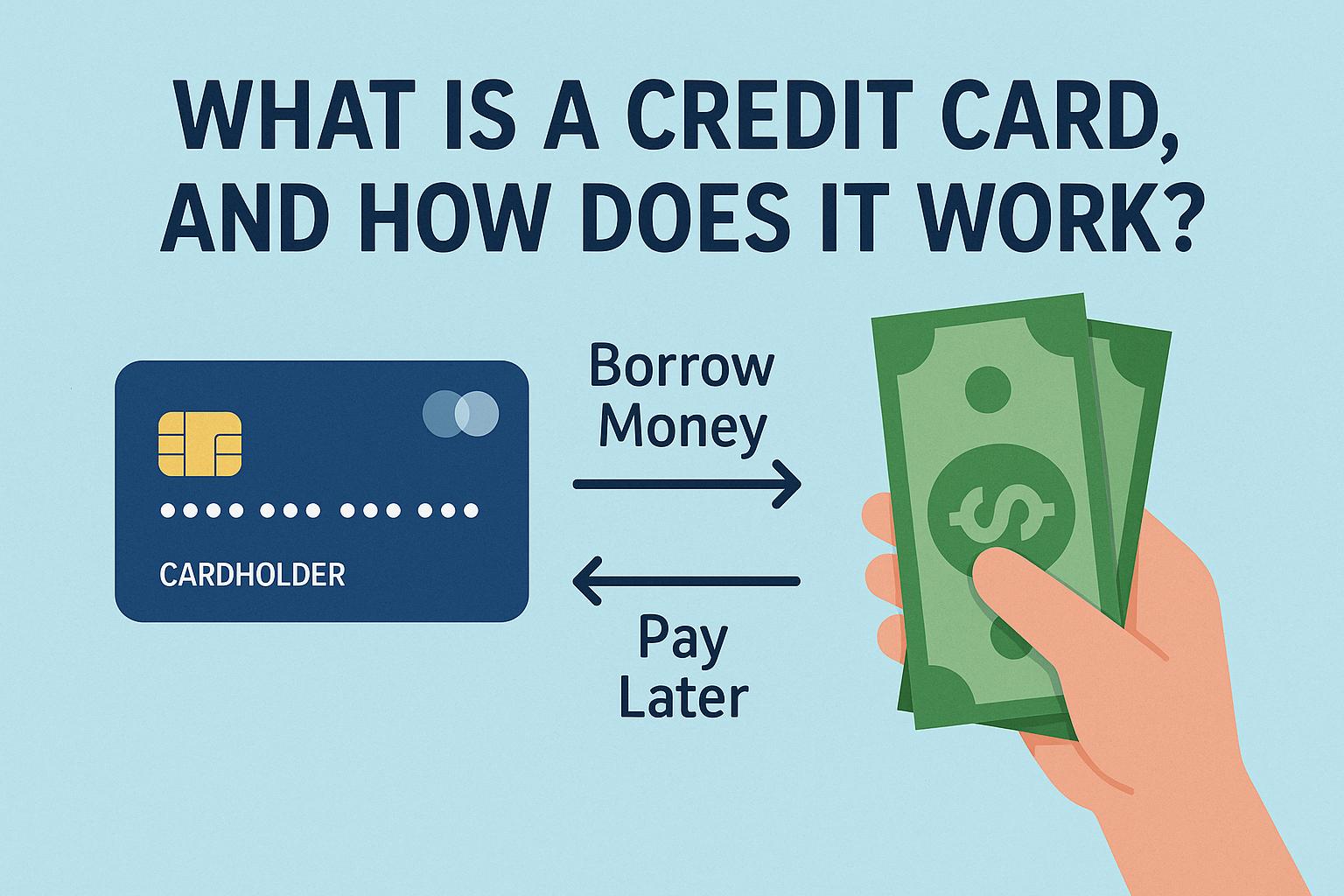

How Credit Cards Work

The operation of credit cards involves a nuanced process. When an individual uses a credit card, it represents a temporary loan from the issuing bank. Unlike paying instantly for items, the bank advances the payment on behalf of the cardholder. Subsequently, the cardholder receives a statement, usually at the end of a billing period, which details all the transactions conducted during that cycle.

If the entire amount owed is settled by the designated due date, no interest is levied on the borrowed sum. However, any unpaid balance rolled over to the next billing period attracts interest charges. This interest charge is dictated by the Annual Percentage Rate (APR), which differs by card type and issuing bank. Having a firm grasp of the APR is pivotal in efficiently managing credit card expenses.

Credit Limit

A significant aspect of credit cards is the credit limit. Each card is issued with a predefined credit limit, reflecting the maximum amount one can spend using the card. This limit is calculated based on various factors, including the cardholder’s income, credit score, and historical credit behavior. Surpassing this limit could result in penalties, and potentially deteriorate the user’s credit score.

Minimum Payment and Fees

Every credit card statement specifies a minimum payment that must be remitted each month. This payment typically represents a small fraction of the outstanding debt. Although settling the minimum payment helps avert late fees, it leads to interest accumulating on the remaining balance. An awareness of various potential charges, such as late fees, annual charges, and foreign transaction fees, is crucial, as these can significantly inflate the cost of using a credit card.

Benefits of Using Credit Cards

Credit cards provide numerous advantages, including the ease of cashless transactions, safeguarding purchases, and offering travel perks. Moreover, some cards come with rewards programs like cashback or points systems. These benefits necessitate responsible credit use to prevent debt accumulation. Using credit cards prudently also aids in establishing a robust credit history, a vital component for future borrowing endeavors like taking out a mortgage.

Security and Safety Features

Contemporary credit cards are embedded with security features, such as EMV chips, designed to enhance transaction security. Furthermore, most credit card companies offer fraud monitoring services paired with liability protection, facilitating the prevention of unauthorized use of the card.

Choosing the Right Card

The selection process for a credit card requires a thorough evaluation of several elements such as interest rates, applicable fees, reward structures, alongside a review of personal financial practices. It’s imperative to compare different offers from various issuers and to carefully scrutinize the terms and conditions. This diligence ensures the selection of a card that aligns with an individual’s financial strategies and aspirations.

Credit cards can serve as potent financial instruments when utilized judiciously. Grasping a comprehensive understanding of their terms, accruable benefits, and inherent risks is essential to leverage their potential advantages while mitigating the risk of falling into debt-related pitfalls.

Effective Credit Card Management

To manage credit cards effectively, it’s essential to maintain a routine of timely payments, which helps in avoiding additional financial charges. Setting up automated payments from a bank account can be beneficial for preventing missed payments. Besides, maintaining an expenditure record helps in sticking to a predetermined budget, averting needless debt accumulation.

Regularly reviewing credit card statements is advisable to ensure all charges are accurate, and any discrepancies can be addressed promptly. Engaging with customer service for any queries or issues regarding credit statements can prevent the escalation of minor errors into significant financial challenges.

Monitoring the credit report periodically is another vital practice, as it offers insight into personal credit standing and uncovers any unauthorized entries. Utilizing free annual credit report services can aid in maintaining vigilant oversight over one’s credit status.

Special Considerations

There are special considerations for using credit cards, depending on circumstances such as traveling abroad or engaging in substantial purchases. Understanding the terms of international usage and whether the card charges foreign transaction fees is crucial for travelers. Some issuers offer cards with no foreign transaction fees, which can be advantageous for frequent travelers.

Dealing with higher-value purchases requires evaluating the potential for purchase protection offered by the credit card. Confirming the card’s terms regarding disputes over purchases or services can provide reassurance and protection in transactions.

In summary, while credit cards serve as flexible financial instruments, they demand careful attention to avoid pitfalls. Prudence in their management prevents negative consequences and maximizes potential benefits, leading to healthier financial outcomes.